Key Pre-feasibility Study (“PFS” or the “Study”) highlights:

- Robust Project Economics: Post-tax net present value (“NPV”) (discount rate 5%) of $871.8 million and post-tax internal rate of return (“IRR”) of 72.03% using a long-term magnesia (“MgO”) baseline price of $1,500/metric tonne (“Mt”) and an exchange rate of CAD$1.00 = US$0.73.

- Production profile: Annual average production of 86,500 tonnes of 98% purity MgO product at capacity.

- Low capital intensity: Initial capital expenditures (“CAPEX”) of $205.4 million including mine preproduction, processing, and infrastructure (access roads and site preparation)

- Competitive cost profile and rapid payback: All-in-Sustaining Cost (“AISC”) of $375/Mt of MgO product, a post-tax payback of 1.5 years, with $1,489 million cumulated cash flow and $871 million discounted cumulated cash flow over 20-year projected life of the project for the purposes of the PFS.

*Based on 250K tonnes per annum of ore throughout.

CALGARY, ALBERTA – November 29, 2022 – West High Yield (W.H.Y.) Resources Ltd. (“West High Yield” or the “Company“) (TSXV:WHY) is pleased to announce the results from its PFS for its high-purity MgO industrial production plant (“the Project“), prepared in accordance with National Instrument 43-101 – Standards of Disclosure for Mineral Projects (“NI 43-101“) with cost accuracy of +/- 20% for the Company’s Record Ridge property located 10 kilometers southwest of Rossland, British Columbia (the “Record Ridge Property“), which is an intermediate-advanced exploration-stage project and is 100% owned by the Company. All figures are expressed in the currency of the United States of America unless otherwise stated.

Kingston Process Metallurgy Inc. (“KPM“), a company based out of Kingston, Ontario, in consultation with KON Chemical Solutions and Tenova (both companies are based in Austria), was mandated to establish the technical viability of a MgO production facility, to prepare plan and capital estimates of the Project, and to provide detailed design and economic evaluation of a semi-commercial demonstration plant, in addition to a high-level design and economic evaluation of a commercial plant at a location to be determined in southern British Columbia, Canada. The financial model of the Project was prepared by Bumigeme Inc., a company based out of Montreal, Quebec based on (i) information provided to them by

the Company, as received from KPM, and (ii) MgO market study prepared for the Company by TAK Industrial Mineral Consultancy (existing under the laws of the United Kingdom). The findings from the aforesaid assessments and models are highlighted in the Study.

Frank Marasco, President and CEO of the Company, reports: “The MgO production Project described by the Study represents extremely positive news for West High Yield and its shareholders. The Study’s completion is a significant milestone on the pathway to production. The results as outlined in this news release make a compelling case for the economic viability of the Project. The Company’s high-purity MgO plant would create a carbon-free alternative to the currently dominating operations in China that are based on the calcination of carbonate ores (mainly magnesite), thus providing U.S. and European end users a green, secure and independent Canadian source of high purity MgO products. The PFS demonstrates the economic benefit of developing magnesium compounds operation in southern B.C. – a mining-friendly jurisdiction with deep mining talent and exceptional infrastructure.”

Study Overview

The Study considered a MgO commercial plant of 250,000 Mt/year ore capacity (the “Plant“), which is based on the installation of five (5) processing modules of 50,000 Mt/year ore capacity (each module called a “Unit“). The Study produced the following information,

- a detailed design and economic evaluation including capital and operating costs of a demonstration plant;

- a high-level design and economic evaluation including capital and operating costs of the Plant; and

- economic analysis of the Plant.

Table 1 below includes excerpts from Table 14 (page 34) of the Study with respect to the capital cost of each Unit.

Table 1: Capital Cost Estimate for the Commercial Plant Unit of 50,000 t/y ore.

| Major Units | CAD$ | US$ |

| Leaching | 6,320,000 | 4,613,600 |

| Precipitation | 5,692,000 | 4,155,160 |

| Pyrohydrolysis | 13,897,000 | 10,144,810 |

| Tank farm | 4,306,000 | 3,143,380 |

| Balance of plant | 2,591,000 | 1,891,430 |

| Buildings | 5,120,000 | 3,737,600 |

| Total Direct Capital Cost | 37,926,000 | 27,685,980 |

| Indirect Costs | ||

| EPCM & Start-up services | 5,408,200 | 3,947,986 |

| Freight | 2,305,800 | 1,683,234 |

| Field indirect & first fill | 1,249,000 | 911,770 |

| Total indirect Capital Cost | 8,963,000 | 6,542,990 |

| Total Direct and Indirect Costs | 46,889,000 | 34,228,970 |

| Contingency (20%) | 9,380,000 | 6,847,400 |

| Total Installed Capital Cost | 56,270,000 | 41,077,100 |

Table 2 below includes excerpts from Table 16 (page 36) of the Study with respect to the operating costs of the Plant.

Table 2: Operating Cost Estimate for the Commercial Plant unit of 50,000 t/y ore.

| Item | Annual Quantity | Unit | Unit Cost (CAD$) | CAD$/year | US$/year |

| Sodium hydroxide | 72 | t | 700 | 51,000 | 37,230 |

| Sodium thirosulfate | 115 | t | 800 | 93,000 | 67,890 |

| Chlorine | 2,160 | t | 500 | 1,080,000 | 788,400 |

| Process water | 262,800 | t | 1 | 316,000 | 230,680 |

| Electrical power | 14,904 | t | 57 | 996,000 | 727,080 |

| Natural gas | 684,000 | t | 4 | 2,501,000 | 1,825,730 |

| Labour | 21 | t | 78,002 | 1,639,000 | 1,196,470 |

| Solid wast disposal | 200 | t | 500 | 100,000 | 73,000 |

| Product bags | 8,640 | t | 15 | 130,000 | 94,900 |

| Maintenance materials | 1,138,000 | 830,740 | |||

| General and Administration | 410,000 | 299,300 | |||

| Total Annual Operating Cost | 8,454,000 | 6,171,420 | |||

| Total Annual Operating Cost per tonne of MgO product | 489 | 375 | |||

The Study considered the capital costs of the Plant to be about $205 million with operating costs of $375/Mt of MgO product, which included mining costs, processing costs, and mine and plant levels general and administrative expenses.

Project Economics

The economic analysis of the Project in the PFS was performed assuming a 5% discount rate. On a pre- tax basis, the NPV is $993.5 million, the IRR is 80.1% and the payback period is 1.34 years. On a post-tax basis, the NPV is $872 million, the IRR is 72.0% and the payback period is 3.5 years. A summary of the Project economics is listed in Table 3 below.

Table 3:Project economics for the commercial plant of 250,000 t/y ore

| Business Results | Project Vlaue | Conditions | Decision |

| NPV of Cash Flow | $871,774,903 | >0 | Yes |

| IRR | 72.00% | >5% | Yes |

| Simple Payback | 1.43 | <5 | Yes |

| Discounted Payback | 1.50 | <5 | Yes |

| Profitability Index | 15.50 | >4 | Yes |

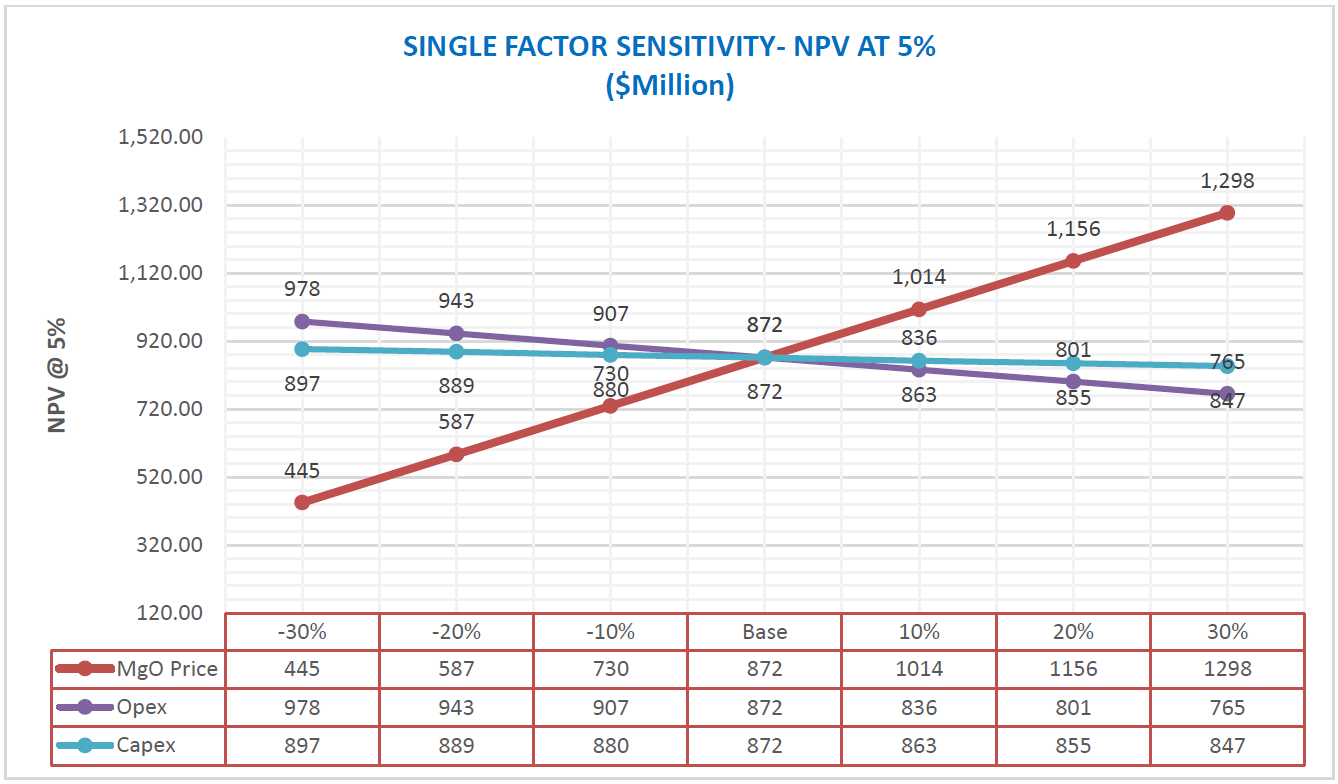

Sensitivity Analysis

A sensitivity analysis was conducted on the base case after-tax NPV and IRR of the Project, using the following variables: MgO price, total CAPEX and total operating cost. The figure and table below (found on page 47 of the Study) provide a summary.

Two-factor sensitivity price and discount rate shows a positive valuation is maintained across a wide range of sensitivities on key assumptions such as MgO prices and discount rate, as in Table 4 below (found on page 47 of the Study).

Table 4: Two-factor NPV (in $M) sensitivity – product price and discount rate

| 871 774 903

$ |

1050 $ | 1200 $ | 1350 $ | 1500 $ | 1650 $ | 1800 $ | 1950 $ |

| 3.50% | 527 859 780

$ |

690 024 438

$ |

852 189 097

$ |

1 014 353 756

$ |

1 176 518 414

$ |

1 338 683 073

$ |

1 500 847 732

$ |

| 4.00% | 498 407 986

$ |

653 474 697

$ |

808 541 408

$ |

963 608 119 $ | 1 118 674 830

$ |

1 273 741 540

$ |

1 428 808 251

$ |

| 4.50% | 470 901 899

$ |

619 323 495

$ |

767 745 090

$ |

916 166 686 $ | 1 064 588 282

$ |

1 213 009 877

$ |

1 361 431 473

$ |

| 5.00% | 445 190 452

$ |

587 385 269

$ |

729 580 086

$ |

871 774 903 $ | 1 013 969 720

$ |

1 156 164 537

$ |

1 298 359 354

$ |

| 5.50% | 421 135 594

$ |

557 490 414

$ |

693 845 234

$ |

830 200 054 $ | 966 554 874 $ | 1 102 909 695

$ |

1 239 264 515

$ |

| 6.00% | 398 611 079

$ |

529 483 798

$ |

660 356 517

$ |

791 229 235 $ | 922 101 954 $ | 1 052 974 673

$ |

1 183 847 391

$ |

| 6.50% | 377 501 374

$ |

503 223 423

$ |

628 945 473

$ |

754 667 522 $ | 880 389 571 $ | 1 006 111 620

$ |

1 131 833 669

$ |

Plant Design

The Study provided detailed design of the demonstration plant and a high-level design of the Plant, which included detailed process flow diagrams and process description, and plant mass and energy balance for both plants.

More Information

For additional information, please refer to the Study available on the Company website and filed on SEDAR under the Company’s profile at www.sedar.com which contains more comprehensive technical information.

Qualified Person

Kevin Watson is an independent Qualified Person as defined by NI43-101 and has reviewed and approved Sections 17 and 21 of the Study..

Florent Baril is an independent Qualified Person as defined by NI43-101 and has reviewed and approved Section 22 of the Study..

Next Steps

Following the release of this PFS, the Company will move the semi-commercial demonstration project forward, which is a crucial step to provide the necessary bridging work for the commencement of the feasibility-level studies for the successful development of the Plant.

About West High Yield

West High Yield is a publicly traded junior mining exploration and development company focused on the acquisition, exploration, and development of mineral resource properties in Canada with a primary objective to develop its Record Ridge magnesium, silica, and nickel deposit using green processing techniques to minimize waste and CO2 emissions.

The Company’s Record Ridge magnesium deposit located 10 kilometers southwest of Rossland, British Columbia has approximately 10.6 million tonnes of contained magnesium based on an independently produced preliminary economic assessment technical report prepared by SRK in accordance with National Instrument 43-101 – Standards of Disclosure for Mineral Projects.

Contact Information:

West High Yield (W.H.Y.) Resources Ltd.

Frank Marasco Jr., President and Chief Executive Officer Telephone: (403) 660-3488 Facsimile: (403) 206-7159 Email: [email protected]

Cautionary Note Regarding Forward-looking Information

This press release contains forward-looking statements and forward-looking information within the meaning of Canadian securities legislation. The forward-looking statements and information are based on certain key expectations and assumptions made by the Company. Although the Company believes that the expectations and assumptions on which such forward-looking statements and information are based are reasonable, undue reliance should not be placed on the forward-looking statements and information because the Company can give no assurance that they will prove to be correct.

Forward-looking information is based on the opinions and estimates of management at the date the statements are made, and are subject to a variety of risks and uncertainties and other factors that could cause actual events or results to differ materially from those anticipated in the forward-looking information. Some of the risks and other factors that could cause the results to differ materially from those expressed in the forward-looking information include, but are not limited to: general economic conditions in Canada and globally; industry conditions, including governmental regulation; failure to obtain industry partner and other third party consents and approvals, if and when required; the availability of capital on acceptable terms; the need to obtain required approvals from regulatory authorities; and other factors. Readers are cautioned that this list of risk factors should not be construed as exhaustive.

Readers are cautioned not to place undue reliance on this forward-looking information, which is given as of the date hereof, and to not use such forward-looking information for anything other than its intended purpose. The Company undertakes no obligation to update publicly or revise any forward-looking information, whether as a result of new information, future events or otherwise, except as required by applicable law.

This press release does not constitute an offer to sell or a solicitation of an offer to buy any securities in the United States. The securities of the Company will not be registered under the United States Securities Act of 1933, as amended (the “U.S. Securities Act“) and may not be offered or sold within the United States or to, or for the account or benefit of U.S. persons except in certain transactions exempt from the registration requirements of the U.S. Securities Act.

NEITHER THE TSX VENTURE EXCHANGE NOR ITS REGULATION SERVICES PROVIDER (AS THAT TERM IS DEFINED IN THE POLICIES OF THE TSX VENTURE EXCHANGE) ACCEPTS RESPONSIBILITY FOR THE ADEQUACY OF THIS RELEASE.